Futarchy: Robin Hanson on How Prediction Markets Can Take over the World

Futarchy: Robin Hanson on How Prediction Markets Can Take over the World

Transcript of interview

I recently had Robin Hanson on the CSPI podcast to talk about futarchy. It’s one thing to spread knowledge on a particular issue, it’s another to invent a new technology to create more knowledge in the world, and help apply it where needed. That’s what I see Robin doing. He convinced me that although it may take a very long time, one day humanity will give less of a role to systems like peer review and unaccountable bureaucracy in determining how we understand the world, and more of a role to prediction markets. The logic is just too compelling. But sooner is better than later, and if you want to be involved, please reach out.

The first step towards this glorious future is convincing people that a world where more decisions are made based on prediction markets is desirable and achievable. In that spirit, below is a transcript of our conversation, lightly edited for clarity. To read more about futarchy, see here.

(beginning of transcript)

Richard: Hi, everyone. Welcome to the CSPI Podcast. I’m here today with Robin Hanson. Robin, How are you?

Robin: Happy to be here and ready to talk about a big topic.

Richard: We’re glad to have you. Before we get started, while a lot of our audience is going to know who you are can you just give a brief description of your background? What do you do? What are your research interests?

Robin: I'm an associate professor of economics at George Mason University. I do an excessively diverse range of things. I just had a paper accepted in a astrophysics journal on the Grabby Aliens. I've done information aggregation. I have two books, one called The Age of Em: Work, Love, and Life When Robots Rule the Earth, and the other The Elephant in the Brain: Hidden Motives in Everyday Life. I guess we'll just find out more about my prediction market work in this talk.

Richard: Do you have a degree in economics?

Robin: No. I have a PhD in social science from Caltech. Caltech has a pretty small social science department with say 20 faculty covering all of social sciences. My degree was in social science. The first time I went on the job market I actually did better in political science, but second time I got this job offer in economics.

Richard: Okay. What are your interests? One of the things I think we're going to spend the bulk of the time talking today is the idea of a futarchy. Is that how you pronounce it?

Robin: Futarchy would be a fancy name for decision markets applied to government. The larger topic would be what institutions can we all share to argue and aggregate information so that we can form collective beliefs that we can act on together? That’s a question in academia.

Robin: It's a question in government. It's a question in business. It’s a very fundamental, difficult problem. I think there's potential for doing a lot better than we've done.

Richard: Yeah. What’s the problem? What do you see as the main issue that this is trying to solve?

Robin: Well, you know most of you have been in conversations all your life. You know that in conversations it’s very complicated. People have all sorts of agendas. They aren't entirely honest all the time and they aren't focused on particular tasks. It's not clear you know that you can believe what they say.

A reporter calls up various expert people with credentials or whatever and gets quotes for them, but they don't have a good incentive to tell their best estimate of the truth in those interviews. They're often incentivized to sound provocative, to ally with whatever political tribe they're with, et cetera. We have these problems all over in all the rest of the conversations we have in business, and government, and academia et cetera.

The question is could we give people more direct, better incentives to actually tell the truth and figure out the truth so that when we had a meeting and people raised hands, and we made a decision what to do we would be doing it on the best knowledge we could have?

Richard: Yeah. The way you answered that question, that made me think of something. Do you see this as a matter of incentives in the sense that whoever the experts are they just have to have better incentives, or do you also see it as sort of a selection process in that there is some trait, or collection of traits that humans vary on, and some people are just better at getting at truth than others? Do you take the first position?

Robin: Both of those factors are important, and so you want an institution that relies on both. You don't want to just take a particular group of people and give them better incentives, nor do you just want a process that selects people. You want to both select people and give them good incentives so that people know when they're selected that they will fact those good incentives and they will be selected on the basis of anticipating that those good incentives will work well for them.

Richard: Yeah. Futarchy is the process of aligning incentives to get better opinions, better policy?

Robin: Well, futarchy is decision markets which is an application of prediction markets in general, which is an application of speculative markets in general. We might say we have this general institution of speculative markets, basically stock markets, commodity markets, betting markets, et cetera. They've been around for many centuries.

They have this remarkable property that they often aggregate information very well from a diverse people. The idea of prediction markets is to use that mechanism on purpose to get better information about particular topics of interest, and then decision markets are prediction markets where the topic is directly targeted at a particular decision, where you're asking about the consequences of a particular choice to make those market estimates and advice as directly actionable as possible.

Richard: Yes. It would be an example of futarchy, say if there’s a bill before Congress. It’s a, say stimulus bill, something in the news. You would have some measure of outcome, the GDP of the country in five years if you pass it or you don't pass it. Then basically the system you envision, basically there'd be a way for the legislators to have their votes tied, or whoever makes the decision tied to the results of the market. Is that right?

Robin: Right. I think it’d be easier to start with like a more personal, smaller scale example before we get to reforming national government.

Richard: Sure.

Robin: I would suggest considering, fire the CEO markets. In ordinary public companies there's the CEO. One of the most important decisions that the board of directors makes is whether to keep or fire the CEO.

The proposal would be to have stock markets that are conditional on whether or not you fire the CEO. An ordinary stock market you trade stock for cash, and the price there is an estimate of the value of the company and all the different scenarios it might be in. Now we're going to make called off stock markets and these are markets where we make trades of stock for cash but those trades are called off, or made as if they never happened if certain conditions aren't met.

We could have a ‘if the CEO stays in power through the end of this quarter’ version of the market. In those markets the trades will be based on the expectation of how much the company will be worth if the CEO does stay. Then we can also have markets where the trades are called off if the CEO doesn't leave by the end of the quarter.

Now this will be markets where people estimate, how much is this company worth if the CEO leaves? Then the difference between those two prices, CEO stays and CEO leaves, becomes an estimate of the value of the CEO for this company. That would be direct decision advice. The board of directors could look at that price difference and say, “Should we keep him, or should we dump him?”

Richard: Is there any legal barrier to a company doing this or someone setting up a market like this?

Robin: Well, there is SEC regulations about commodities. This could be thought of as a stock derivative. You need some sort of permission there. That's the main regulation limit. Of course you'd also need the board of directors in the company to be interested in these numbers. That's more the real limitation.

Richard: Yeah. But it seems like you don't need to convince that many people as long as, putting aside the regulatory issue. If you have a corporation, presumably if the system of markets being better than other kinds of decision making is right they should have a huge advantage right, in the market? They should be able to make a profit and their business should do well.

Robin: Our consistent experience with speculative markets is that when we compare them to other mechanisms like polls or committees they’re either about the same or substantially better. They’re almost never much worse. Sometimes the question is just easy, and any mechanism can give you the answer, like is the sun shining right now or something like that right?

Everything will just tell you the answer. But then sometimes things are hard or complicated, and then existing institutions are doing a bad job. In that case the market can cut through and give you a better estimate.

Richard: Okay. I get that. But then the question is wouldn't you just be able to... I mean you should be able to do this and then you can just have a tournament for your CEOs right? You could have 10 different prices right? You can just see the best one…

Robin: Right. This conditional market mechanism hasn't actually been tested out in the world outside of the laboratory tests in that we haven't been able to get people interested enough to try it. We've had a lot of tests of speculative markets that aren't conditional in the sense that we've had markets on deadlines, whether you make a deadline in sales and things like that.

We've probably had 100 different trials like that over the last few decades. Typically what happens is that if there's enough support for the market in order to induce an affectivity then again the price is about as accurate or more accurate than the status quo and most users are satisfied. The costs are modest. That's been the history for many decades.

However a key problem is usually the market gets killed in the sense that an organization says to stop and doesn't continue it. The main reason is that it's relatively disruptive. These markets are politically disruptive. The way they are disruptive is analogous to, imagine you put a very knowledgeable autist in the C suite, that is somebody in the C suite that knows a lot about the company and they go to the meetings. They just blurt out when they know things that it's relevant to the conversation but they have no political savvy.

They have no sense of, what does anybody want to hear, or who will be bothered by anything they say. That sort of an autist would not last long in the C-suite. They would be shunted aside and become an advisor to someone perhaps, trusted advisor to their side but they wouldn't be allowed to speak in the boardroom. But that's what a prediction market is. It has no idea who wants to hear what it has to say.

It will often say things that people do not want to hear, and that embarrass them, and that contradict what they've said. Then all the worse of course it will be proven right.

Richard: Yeah. But what's stopping the autist, or I guess what's stopping them is nobody has just done this yet? But theoretically you could imagine the autist setting up the rules for the corporation, right?

Robin: You might if they were in charge at the beginning sure.

Richard: Yeah. That's what you need. You need one rich autist interested in these ideas. He would go in and he would say the board has to operate according to these…

Robin: Now we move to the question of like, what fraction of companies out there are actually maximizing profits?

Richard: Yeah.

Robin: It’s a very basic question in economics and in our world. We economists tend to assume as a simple initial working model that organizations that are for profit actually do maximize profits. That's the thing they usually do. If you give them a choice of A or B, and B is higher profit they'll choose B.

Here if you apply that model you say, “Well, this looks like it would give them key information to make key decisions like, ‘Will we make the deadline,’ and it will be valuable. The cost is relatively low so of course they would do it.” That's what you would say if you were applying that theory. Then here we have a case where it looks like, well it hasn't happened yet.

You might think, “Okay, innovation is slow. It takes a while,” but we’ve been waiting several decades. Honestly if I look across a wide range of other areas of corporate behavior I can't fully support this profit maximizing theory. I think I can find a lot of other places where what they do does not maximize profits.

I could give you a long list of examples. We could go through some of those but then the question is, “Well, how do I come to terms with it? What theory do I have affirms in the absence of profit maximizing to explain the behavior?”

Richard: Yeah. Well, actually I like the idea of going through the list. Besides not operating according to betting markets what leads you to the position that corporations don’t maximize profit?

Robin: Well, of course until recently we appeared to have too little remote work. Most commenters had though remote work should be much more widely adopted and it hadn't been. We also have the standard story of too many meetings. Almost everyone in large organizations complains there are too many meetings with too many people in them that last too long, yet they keep happening.

We usually have too many people interviewing new candidates as opposed to just looking at their credentials on paper. We often have, when a new person becomes the boss of a group of people usually some of the people they're the boss of they inherited, and some of the people they get to pick. Usually they give higher evaluations to the second group of people and everybody knows that.

But they leave that on the books. We let them do that. There is a standard not invented here bias where we're not so interested in stuff that wasn't invented here compared to stuff that was invented here. There is yes man bias which is of course famously well known that if you're a manager and you’re trying to get people to tell you the truth about things one powerful strategy is to ask them what they think before you tell them what you think, and then use what you think as a way to judge how good what they think is.

Even if you're not very well informed compared to them it still can give them an incentive to tell you what they think because their best guess about what you think is still whatever the truth is. However many managers don't follow this strategy. They very clearly telegraph what they think and therefore induce other people to be yes men, or yes women, where they just parrot and repeat back what the boss said so that not longer produces an incentive for the people to think carefully about what they think.

It instead gives them incentive to parrot what the boss says. These are a half dozen examples here but I have a blog post somewhere where I went through 20 of them. Again we go down the list and we go, “Each one, if it was just one I might say, ‘Okay. I just don't understand that somehow. I'm not looking at it right. Somehow it really is profit maximizing.’” But if I've got a list of 20 of these things and they're big things I go, “Well, I guess I need a better theory.”

Richard: Yeah. Okay. What is the alternative theory?

Robin: I'd say that we want to think of large organizations as fields of battle between coalitions, but that each coalition is fighting for control over the organization, and most of these policies are in the interest of individual coalitions. They're just not in the interest of the organization as a whole.

For example, in a coalition you want lots of your people in the meetings so that they can push for your agenda. It's great if the other people aren't in the meetings, especially if say they're remote working and they can't make a lot of the meetings, so you want the other people to be remote and not in meetings and your people in the meetings.

You want your people to be interviewing new candidates so they believe that they owe you a debt of gratitude if you're hired, et cetera down the list. When coalitions are competing with each other there's policies that help coalitions which isn't so much what helps the company. Related to prediction markets or forecasts most coalitions are organized around a set of shared interests and they form an agreement to support certain projects.

They just don't want their agreement to support those projects to be at risk to fluctuating estimates. Prediction markets will fluctuate right? At the moment it might favor something and then a week later it might change its mind right? That's just not very reliable as a member of your coalition. You want to get together and support George's project, and George's division. Then you want to do that early on and stick with it regardless of how the estimates change.

Richard: Do you think this is what happened? I'm sure you've seen the charts showing for example in universities administrators, the number of administrators are going through the roof and the number of professors is flatter, just barely rising. I saw another one with the same thing with doctors versus medical administrators.

Then someone on Twitter said that chart was no good. I'm not sure if it's good or not, but do you think as a general matter this is what's happening? Perhaps there's this administration bureaucracy that's where this coalition is getting bigger and bigger and it's just expanding because it's optimized for its environment?

Robin: It's not a crazy theory but I haven’t thought that through. The question is if I had a coalition in a university for example would increasing the number of administrators within my part of the university help me win coalition battles against the other ones? If yes, then the theory is predicting that this happens, but it's not obvious that that’s true. But I don't know university administration as well as other people so maybe someone who knows that can comment.

Richard: Yeah. Is this just a matter of it’s when institutions get too big? Does your theory predict that the smaller the corporation, if you have a founder for example, just a founder of just a few people, that they’re going to behave more rationally than a larger corporation that's been around for a while?

Robin: That’s not my theory. That's just very widely predicted. Almost everyone says that small organizations have fewer of these coordination problems. They have other problems. There’s a lot of problems that bedevil smaller organizations. Often it’s just like the leader is arrogant, or blind and has all sorts of just personality issues, etc. Right?

Robin: That tends to be the problem you have with very small organizations is the very personal conflicts. But at least you don't have these larger coalition battle problems.

Richard: This is a problem it seems like. This theory would go... Well, let me ask you this way. What's wrong with the classic free market position that what will happen is you'll have varying degrees of rationality and the ones that are the institutions, and firms, and individuals who are rational will just out compete the ones who are not? What do you see going on there?

Robin: I mean I think in fact the correct response is to say the free market version is probably the best. You just have no idea how much worse things can be. People often look at the status quo of a business world say that is relatively free market. They look at this up close and they go, “This looks terrible how could you possibly be defending this?”

The argument has to be, “Well, it would just be so much worse without this.” And in fact often if you look to large stable organizations like universities and government agencies, or churches that have been around for a long time it is in fact worse. I think that's roughly right. Another story might be we've hobbled some of the competition between firms that might solve some of these problems.

I honestly think one of the biggest wins we could do is to just allow stronger hostile takeovers. The laws at the moment make it harder to do hostile takeovers. They require a substantial tax on them in essence. If you see a badly run company and you have an idea how it could be run better the problem is how are you going to profit on that? But if you could just buy up the company, change its management and then sell it again after it was better that would be a big, powerful engine for making it better.

There have been times when that mechanism has been allowed to do more and it has made huge changes. That's what inspired people to lock it down and prevent those changes because they were scared it was coming for them.

Richard: Yeah. There's just this status quo bias. What's the regulatory barrier there? Is it antitrust, or what is it that makes it difficult to do this?

Robin: The key thing is that when you are going to try to do a takeover bid you have to warn people so they can bid up the price on you, which means that you end up paying a substantially higher price, 20%, even more above what you would have paid if you could have bought the stock in stealth without people knowing you were trying to buy it up.

Richard: Where do you... This is a technical question. How do you announce it and what happens if just some other….

Robin: Well, there is a formal process by which you announce that you have a certain number of shares in the company and that you're hoping to buy more. Again you can't have bought very many of them by the time you announce this. Then what typically happens is the prices get bid up in the expectation that you'd be willing to pay more for the company.

Then you may or may not succeed in buying it up. There's also a number of other things we allow such as poison pills, various rules in which if there's a takeover then all the sudden some people get some extra stock, and some extra voting shares, and some extra abilities to make it hard for you. We have a whole bunch of these rules that have basically made it difficult for people to take over companies.

Richard: Yeah. Your view is basically irrationality persists, irrationality as in non-profit maximizing behavior, and then presumably that's hurting the aggregate wealth of society. That exists because basically we're protecting institutions. We have a status quo bias-

Robin: Right. We're making it hard to make changes. On the other hand competitive business world is one of our best worlds we have in our world. It's one of our shining examples of productivity and innovation is the business world to the extent that it is free to do something. Now you could just say, "Well, if we make it more free to pursue profits and to innovate then it could be even so much better."

Richard: It's funny because you say this is the best world we have when you compare it to other things. My background is in international relations. People often start with the assumption that the country is trying to maximize something…

Robin: Right. That's even crazier an assumption, presumably it's even easier to find counterexamples to that.

Richard: Yeah. I would go further and say it's harder to find you know…

Robin: Examples of it happening.

Richard: Yeah. Exactly. Why doesn't the US just..

Robin: Right. How many wars were started that were actually expected profit wars for example?

Richard: Yeah. They tend to be pretty crazy. The whole field to a certain extent is sort of built around... Of course that's not how everyone thinks.

Robin: Right. But in the future we could imagine for profit, for company nations for example. Might imagine that it would be possible to make better run nations and that they would be more rational in this sort of selfish, strategic sense. That's a thing that could happen in the future. In some sense futarchy is this proposal to use decision markets for governments and it could in fact achieve that. Maybe we should say a bit about how that might work?

Richard: Do you put futarchy in a larger intellectual tradition? Because a lot of people when they're coming up with an idea... Did you come up with this term by the way?

Robin: Yeah, and I've been ridiculed for it. It has various associations in different languages, et cetera, but I was just thinking of it as a future government. That was my origin of the name. And yet of course the context, there's two key contexts. One is to show how far the idea could go if you just talk about, say firing CEOs or changing churches, or all sorts of smaller organizations. I don't think people get quite as inspired as if they could see how it could become a form of government, because that's pretty grandiose and high status.

Futarchy is trying to show how it might look if you went all the way to that level of application. Not that I'm recommending that we do that first at all. I would recommend we try small scale experiments and work our way up to large organizations, but still that can be an inspiration to go down the path because you hope you might go that far.

Of course it's also related to other proposed forms of government and so it has some differences and similarities to others. You can think about what it's emphasizing and what its problems are compared to the others.

Richard: We put aside, we started with the markets for CEO performance. Could you talk a little bit about the broader, the grander idea? How would your ideal government function?

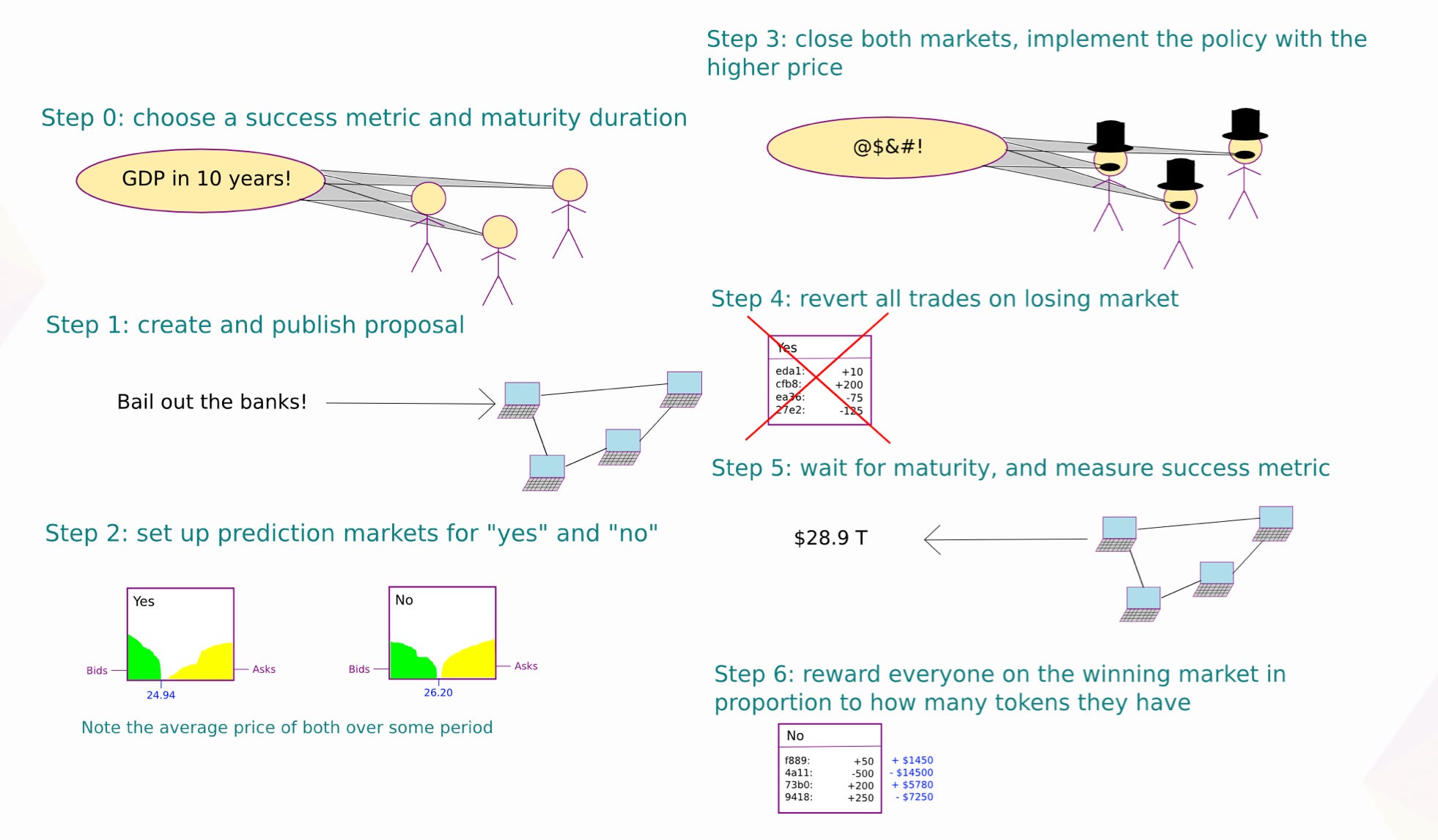

Robin: In the CEO case we have an outcome that we agree on that's the relevant outcome, IE the stock price for this public company. Then we have discrete decisions. Do we fire the CEO or not? That's the key things we need to make this apply to other things.

For a national government say, the discrete choices would be each new bill that's proposed. We'd be asking, “If we pass this bill are we going to be better off?” Then for the outcome we're going to need to construct it more for a nation. The idea is the legislature still exists but now they vote on bills that defines a national welfare function.

It's a bit like say GDP at the moment, say the Bureau of Labor Statistics defines GDP and then it oversees the measurement of GDP. Of course many scholars often look at GDP numbers and say that the countries with higher numbers are better, and try to recommend policies that would increase your GDP.

Well, now we’re going to authorize this same sort of agency to estimate number like GDP except we’re going to tell them to put more things in the number. Bills before Congress would say, “Count more trees, and count leisure, and count international reputation.” They would just make a bigger formula that included all the stuff they cared about in this measure of national welfare.

But now there would be assets, financial assets that pay out in units of national welfare. If national welfare ends up being 12.9 then it pays out $12.9 or some other financial unit. Now we can then bet on national welfare. But more importantly we can bet on national welfare conditional on whether a particular bill passes.

Then for each bill we'd have these two prices, the price of national welfare if the bill passes and the price if it doesn’t, and then the difference between those two prices is a direct advice about whether or not to pass that bill. We could set that on the side and just have it be giving advice to a legislature, or we could put it directly in charge and just say, “When the market approves of it by having a higher price then that's just as if the legislature had passed it and it just becomes law.”

Richard: To just make sure we’re clear let’s say we’re debating Obamacare. Then we would have to first have sort of an aggregate measure right? We’d say, “What's GDP going to be?” Maybe give that like 40% of the calculation. What’s the human life expectancy in the US going to be in 10 years or whatever. Then you would just do this for a bunch of different things. Then you would just have a market, basically say, “Okay. If Obamacare passes it's going to be X, and then if Obamacare doesn't pass it's going to be Y,” right?

Robin: Right.

Richard: And then…

Robin: This national welfare function, we don't have to redefine it for each new bill. It's just the standard welfare function that we have for all the bills we consider. Then sometimes we'll change the welfare function and then we're changing our metric of consideration. But basically we might have say two slots of day where a new bill is considered by this process, or might even have say 10 slots a day.

At each slot we might even have an auction to decide who gets to put their bill up during that slot. Then during that hour say, or half day, the market decides whether that bill passes. Then we go on to the next bill, and the next half day. Again the national welfare measure would just be the same measure that we had decided on months ago.

Richard: Yeah. Okay. You don't need the ascent of Congress to do this?

Robin: Right. If you want to just make it be advisory you would just need the legal permission to create these markets, and then we can just sit on the side and we could track say, when the Congress passed a bill versus didn't pass a bill did it follow this market advice, and see the net effect of these things. But it would be better for many reasons if it was just more directly in charge.

Richard: Yeah.

Robin: We already have a democratic system where there are often experts who know the right thing about bills and they tell each other the right things. The public never hears that and so politicians just ignore it. The question would be if this was just on the side as an advisory thing would the public pay any attention?

Richard: Yeah. How serious are the regulatory barriers? I mean if you had enough money could you do this for the things that Congress is debating right now?

Robin: Well, I wouldn't do this as the first thing. Again, this would inspire you as an end point that you could eventually get to, but a shorter term project would be say in a presidential election you've got the Democrat or the Republican who might be president. We could just estimate some outcomes for the nation conditional on whether the next president is Democrat or Republican right?

We could have GDP. We could have life span. We could have war deaths. We could have all sorts of numbers and that would be a straightforward thing to do every presidential election. We could just be estimating the consequences of who we elect. We really haven't done that before.

Richard: Is that the best way to do it or is that going to pose difficulties? Because if the market comes back and it says Democrats are unquestionably better for the country than Republicans or vice versa that’ll poison the idea of having markets with half the country wouldn’t it?

Robin: Well, you will want to collect a track record over a longer time. My overall plan is that I want these things to happen in small organizations to get track records there and then slowly work their way up to bigger things. We don't want the only main trials to be national level politics. That doesn’t make sense because you don’t even really get enough data there.

You want a lot of smaller decisions where you get a lot of data and where you can show that this is just working well. Think of it like... I’m old enough to remember a time when the government started to use computers for things. They did that because the private sector was using computers for things and people said, “Hey. Why isn't the DMV using computers if the private sector is?” They got kind of embarrassed and they decided they would try to use computers right?

Because it was just obvious that elsewhere this was a pretty good idea. That's how you want to do innovation ideally is you just want to have lots of people using it because it just seems to work. Then eventually the government is shamed into doing it too.

Richard: Yeah. Do you see opportunities out there besides the CEO markets? What else could be promising places to do this?

Robin: This mechanism really is quite general and it can apply to a very wide range of problems. I would basically mainly be opportunistic about where there's a group of people who are willing to try it there. But just to whet your appetite we can go over a lot of options here.

Most organizations hire people regularly. Each time they have a job opening they usually interview several people for each job. When they hire them for that job they're hoping for certain outcomes. Usually they have some internal process that rates how well that employee is.

They could in two or five years have a rating for that new employee of how well they did. It would be straightforward then to have markets on each candidate for a particular job position saying, "What will be the rating of this employee if we hired them in, say two or five years?" That could just be a general process every time you had a candidate for a job opening.

Of course every time you got a project with a deadline you should have a market on whether you'll make the deadline. You could even have that market on whether you make the deadline give you that probability conditional on changes you might make to the project, i.e. pull back on the requirements. Add resources.

Those are all sort of obvious... Change who's in charge of the project. Those are all obvious things you might do to see if you can make a deadline. Students who are high school students applying to college could have markets saying if they chose college X, what will their outcomes be say after they... In five years, or if they chose college Y.

The markets could tell them which college to pick. Or on the other side of the equation the colleges could have markets in the student applicants saying, "If we accepted this applicant how well would they do after four years here in our program," say.

Richard: Who would be betting on, for example the individual kids going to one college or the other? Their friends and family or how does it [work?

Robin: Well, so for all of these markets there's a key question of who do you allow to participate? One of the issues there is that whoever you allow to participate gets to see the information and the market prices. They're also the people you want to reveal information to so they could be better informed at making choices.

If you had a student who was willing to let the world see their test scores, and their application essay, and even some description of their priorities or whatever, maybe personal information, then you open that market to the public. Then people could browse that material and make a guess about that particular person.

There's a trade off though. If they don't want to reveal as much information about them then they don't have to, but then fewer people in the market will be able to make a good judgment and they will just be degrading the quality of their estimate as a cost of keeping some privacy. You know that's completely reasonable to do but you just want to make that trade off.

Another application that would probably be even more disruptive is when you're thinking of marrying someone and you ask the markets, “How would our marriage go if we get married?” Or you could even think of dating particular people and ask, “How will it go if I date this person?” Those are things of course you would mostly want to be asking people who knew you somewhat better, but the whole point of these markets is you don't have to decide who's good at answering questions. You just open it up and you let them decide.

Richard: I think in that case in particular there’s such an informational asymmetry between you as an individual and everyone else in the world, that if there's one place where a betting market is made that you can not improve on just people making their own decisions about the marriage, and dating, and things like that.

Robin: Now other people who were in that market would want to know if you were betting in it too. There's a general phenomena in these markets where people should be wary of betting against people who know a lot more than they do. This is, for example, one of the rationales for limitations on insider trading and stock markets.

There are many reasonable choices to make there. You could tell the world, "Well, I'm going to be betting in this market on whether my marriage works but you're welcome to bet too." They might think, "Well, I don't know as much as you do. I'm not going to touch that." In order to get them to bet you might say, "Well, I'm not going to bet on that and neither is anybody in my family," right?

You could just set a limit on who's going to be allowed as a way to entice people farther away to participate. Similarly a company who has a stock market on that company, if they could choose to allow insiders then they'd have a choice. If we allow insider trading then people who are not insiders will know they might be trading against insiders and then that might put them off from trading on that stock.

Or on the other hand if we allow... If you prevent the insiders from trading we will entice more outsiders to trade. On the other hand we'll lose the information those insiders would have given had they been allowed to trade.

Richard: Yeah. That makes me think. Do you have an opinion on laws against insider trading? Do you think that they're generally good or bad?

Robin: Well, it seems to me that it's the company that has the cost, so it's not clear to me why anybody else should be having a say. Whoever owns the company is making the trade off in whether to allow insider trading. Now, of course if the company is not being run in the interest of those investors then we have to worry about making good choices about insider trading, but then we have to worry about making a good choice about everything the company does.

That's what we were talking about before when companies were not run for the maximizing profits then the investors have to worry about what they are being run for, and whether they're going to be basically stolen from the people who are managing things. But insider trading is one way they could be stolen from. But there's 1,000 others.

Richard: Yeah. One place where this might really work is I think sports. This is something that you could get a lot of people betting on because people love arguing about sports. You could have a thing where you have the NFL or NBA draft and people always debate should you draft this player, or that player? You could have markets easily based on how many wins…

Robin: Sure. I just happened to have a conversation with someone on that a few hours ago, but it's still an idea that's going to happen some day. When people say betting on a football game today, you’re betting on who's going to win the game and say by how many points, but you might have more fun betting on each play.

That is not only betting on what the play will be and how it will go out but recommending on the play. You could say, “If we pass this play how many yards on average will we get? If we run this play how many yards will we get, or what’s the chance of making a first down?” You could bet on the consequence for each play.

Similarly in a basketball game you could bet on taking out a player, putting a player in. In a automobile race you could bet about when you make a pit stop, when you don't. There's all these choices in games and I think people would find it more engaging to bet on recommendations for choices in the game.

Richard: Yeah. Yeah. You can already with the sports betting. If you go to the websites you can bet for example not just on the game. I don't know if you can do conditional bets. I have never seen that.

Robin: Right. I’ve never seen conditional bets on choices.

Richard: Yeah.

Robin: That's the key thing here, the choice of a player or choice by a coach.

Richard: I've seen stuff like who will win the tip off in basketball, and who's going to win the coin toss in a football game? Who's going to win first quarter?

Robin: I once looked onto doing this for war college war games. As you may know many war colleges have war games where they put teams on different sides and give them various equipment in a simulated war. They have them go to war. You could imagine, well letting everybody else who’s watching the war game give advice about particular strategies in the war game. That seemed plausible to me but then when I talked to people at war colleges I found that most of these war games are kind of fake.

Richard: Yeah.

Robin: They have a predetermined outcome that’s some lesson they want to tell, and so they aren't really letting it be open to winning one side or the other.

Richard: No, that's funny because you'll see headlines every now and then that'll say, “Oh, my God. The US loses to China in a war game,” and yeah I always thought that that’s…

Robin: I’m sure there probably are real war games somewhere. They just aren't at the war colleges. That's where I was thinking I could convince somebody to try this sort of thing.

Richard: Yeah. Have you had any partial successes? Are there projects that are getting off the ground that you are excited about? Have people taken up your ideas anywhere?

Robin: Well, there's been a whole pile of work in blockchain where people have created prediction markets on platforms and tools on various blockchain systems. Unfortunately most of that work has been at a low level of tools and platforms so they haven't really gotten very close to the applications. Blockchain people are just mostly software people and algorithm people.

They're not so much business people who work with particular clients. They just haven't been very eager to get their hands dirty working with particular customers who might want to do markets and particular things. But they've still been collecting all these tools and so hopefully some day somebody will use all those tools to connect to the customers.

Richard: What is the advantage of the blockchain? What is the difference between a blockchain say market versus just something like PredictIt?

Robin: Well, that's an excellent question. Initially the story was that blockchain was out of control, that it couldn't be regulated so you could set up a system on a blockchain. If the regulators didn't like it they didn't have anybody to go to stop it. The blockchain just kept going regardless of who didn't like it.

That was a big selling point. People said, “Well, look at all this financial innovation we can do because we are free from existing regulations on the blockchain.” That's what they said, and then a lot of companies formed on this basis.

But these companies didn't take personal strategies to match that rhetoric. You would think if your plan was to put a product on the blockchain and that you were going to say nanny nanny to the regulators because, “You can’t get me,” you wouldn’t have a big public presence with the headquarters, and your picture in the magazines, and show up in person at conferences right? Because…

Richard: Yeah. Sure.

Robin: ...well, that makes you more obviously a target right? That's what they did though, and then they sort of back pedaled and said later, “Oh, we're following all the regulations.” But you know people don’t really believe that. It's been this big question, to what extent will governments crack down on these blockchain things that at least from the government regulators point of view are not following their rules?

Richard: Yeah. Do you have in mind the Coinbase news that had come out the last few days, or was it today or yesterday that-

Robin: This is just a continuing issue. I don't have any particular recent event in mind but there are lots of stories about regulators thinking of doing a lot more regulating and cracking down more. This is a big question about blockchain is how far will they crack down, and what will be the consequences? Of course people say, “Well, in principle Bitcoin can keep chugging along even if they do crack down,” and no doubt that's true to some degree.

But the question of how much activity there'll be is still somewhat open. You could have it chugging along with a far lower activity because a lot of people have been discouraged.

Richard: Well, yeah. Just for the listener we're talking now on September 8th, 2021 so who knows when people will be listening to this. There's been just news in the last few days about Coinbase, and the FCC, and I don't know all the details but it's something like that…

Robin: In the last few months China had this big policy of saying, “No more mining here.”

Richard: Yeah. Exactly.

Robin: There was a big drop I believe in prices right at that point reflecting the fact that people then realized there'd be a lot less stuff happening in China.

Richard: Yeah… that wasn't reflected in the fact that Bitcoin has been doing pretty well recently right? It was apparently not fatal, or not that bad for Bitcoin right?

Robin: The volatility of these prices is so large that I wouldn't draw much of any inferences from the price movements. It's just wild.

Richard: Yeah, but the price for Bitcoin has been doing well right? Isn't that an indication that whatever the Chinese did it wasn't hurtful to the longterm prospects of cryptocurrency?

Robin: Well, the volatility of these cryptocurrencies is just really large, so that makes it hard to draw many connections between particular events and what's happening with it. That's an issue about these conditional markets. People have noted that if you have a stock market sequence and then you have events you can try to correlate events in the stock market sequence in order to untangle conditional estimates. For example people have tried to do that with betting markets on elections in the stock market in order to say which candidate is better for the stocks by looking at the correlation between those prices.

It's possible to do but the price movements are noisy and so there's a lot of room for arguing there. Just the direct conditional markets are a much clearer signal than these correlations in prices.

Richard: Yeah, there's noisy but there are a lot of elections right? I mean you could even do things like in places that are... You have all the national elections right every two years, and then you have even local elections when you have mayoral races. I guess there's not a lot of…

Robin: Right. You just don't have betting markets in all those races.

Richard: Yeah, but you have corporations that are located there for example-

Robin: Sure.

Richard: ... or industries there. It seems like you... Anecdotally it seems that... I remember. Do you remember Bernie Sanders during the primaries? He won some primary and then he said, “Oh, the...” Or he lost a primary. He lost and then he said... I think he lost a primary and then the market went up. Then his argument was, “Look. These billionaires are so bad.”

Robin: “I’m bad for business and that's the way I want to be.”

Richard: Yeah. He was proud of this. Given the political culture it was the other way around. He might have won and it went down. I don't remember. I think he lost it though.

Robin: A standard story in finance for a long time has been we've got thousands of market prices in the financial world, and there's all these events that happen in the world so in some sense there's really all this information embodied in all these financial market prices, especially if they fluctuate every minute or so.

In principle the answer to all your questions is somewhere out in this vast cloud of financial market prices. That may well be true. It's just not at all transparent. You'd like a clearer answer. A thing that betting markets can do is give you a more direct, clearer answer even if in some sense that answer was already implicit in all the other prices.

Richard: Yeah. I think transparency is key because if someone is doing this research on the effects of stocks in the market of election outcomes I would think they’re probably on Wall Street. They’re probably not in political sciences departments. Would that be your intuition too?

Robin: I mean they're in both places, but again you know there's so much dispute, I mean there are so many interested parties that with statistical analysis it's just possible to do it so many different ways to get the answer you want. I'm sure if you're in the know you could know who was playing those games and who's not, but the rest of us from the outside find it harder to tell.

Richard: Yeah. But your idea of incentives and people getting things right I think would give you an intuition that people playing the stock market are doing better than political scientists, or you don't have that intuition?

Robin: I mean it’s definitely true that there's a lot of very smart people playing stock markets and financial markets, and that a lot of them make money. But they mostly make money from the other people trading in those markets which has to be a warning against ordinary people trying to go out and speculate on these things.

That would be my biggest advice is if you’re going to play the stock market you should be part of one of these organizations who really knows what they're doing. Because if you go out and just try to bet against them most likely you're going to be on the other side of their trades and losing.

Richard: Yeah. Okay, yeah. This is all interesting. It seems like you’re saying it a little bit differently because... Two different things. Because you're saying that you want to start big with the government because it's high status and you want to start from there, but you're also saying we could start somewhere, maybe sports leagues or something.

Do you see the big thinking as a way to incentivize people and just get people excited about this stuff? But do you think practicality people have to start a little bit smaller?

Robin: Definitely just pointing to the big applications can inspire people even if you’re not going to do them first. Making that connection to people can make them more interested. This is also true for many kinds of innovation. Most kinds of startups or companies you'll have each person doing a pretty small think, but you'll want to tell them about how that's connected to the big project of the organization.

That makes them more interested and motivated to be part of the whole project right? I definitely... For the purpose of collecting data and getting solid progress I'd rather do small things first. On the other hand I do think there's this interesting status strategy of starting from the top down. I don't know if you remember the movie The Social Network which is about the early days of Facebook.

The story was there were other social networks before Facebook, but they started with average people and then had an average pool of people you could connect to which wasn't nearly as tempting as Facebook because it started at the very most prestigious place, Harvard, and slowly it worked its way down the status hierarchy adding Yale or Princeton. Then at each point as they expanded it people were eager to join because they were eager to associate with these higher status people.

The general lesson here is it’s often if there’s a status barrier to doing something it’s easier to start at the top and work your way down. I think firing the CEO is a example of starting at that top. If we think about all the different decisions companies make it hard to find a more prestigious and important decision than firing the CEO.

If you could just directly legitimize using speculative markets to make that decision you would have indirectly legitimized lots of other decisions, because people would say, “Well, if you can use that to fire the CEO you could use it to fire the CFO,” right, and CIO?

Richard: Yeah.

Robin: Then maybe to regional manager, and maybe to pick an ad agency right? You’d work your way down the less prestigious decisions but each one of them you could have said, “Well, as long as you’re willing to use it over there why not here?”

Richard: Yeah. You mentioned these things backfiring, so for that specific example, The Social Network, I mean if you’re in politics today and you say an idea came from Harvard that’s usually I think a negative signal. I think most people say that’s bad, or at least they pretend to think that.

It could have the opposite effect I guess. If betting markets become something that people in Washington do and they’re a little bit too complicated for normal people to understand there could be a backlash. Do you worry about that?

Robin: Yeah. Let’s talk about the public perception of betting markets and what sort of attitudes there are to them, and issues with public reaction. I was involved in a publicity fiasco in 2003 when I was part of a DARPA project where we had a research project set up to create betting markets on geopolitical events in the Middle East.

Then on a Monday morning two senators had a press conference where they declared that this project wasn’t going to be betting on death, betting on terrorist attacks, and that was terrible. Then by the very next morning after that the secretary of defense in front of Congress declared the project dead.

In those 24 hours they never asked us if the accusations were correct. They didn’t need to because it was such a tiny project. Why bother to even think about defending it? But that shows that many people have some mental rules about, they don’t think you should be betting on death. That’s just not appropriate. It doesn’t matter why you might be doing that right?

People have some things they might be uncomfortable with betting on and that’s a thing you should stay away from is betting on death, say. But you’ll notice that most of the business press tends to report news in terms of financial market price movements, and they don’t tend to question those movements.

They try to explain them but they don’t question them. If the price of IBM goes up the reporters don’t say, “Well, that was a mistake. It should have gone down.” They might say it went up because of this or because of that, but that’s most accepting the prices as good estimates and then trying to explain them.

Now sometimes people will tentatively say, “Well, maybe these things are too high there or too low here.” But that says that in the business press at least people do defer to financial market prices as sources of information. Then the potential that could apply elsewhere in society there is a lot of deference given to financial market prices in a wide range of contexts.

Richard: Yeah. Yeah. I guess it depends on how sophisticated your audience is. It’s funny. You mentioned the people don’t like death markets. There was at PredictIt... There’s all those markets, will Bashar al-Assad or will Kim Jong-un be in office by this date?

There was one on Kim Jong-un last year. That’s basically, will he be still the leader of North Korea by the end of 2020? It’s basically a death market because there’s not much chance of him getting overthrown, or voted out, or anything. There were some rumors about him having bad health. He was out of the public eye for a while.

There were rumors that he was dead in the press. The market got down to something like 50/50. I remember I bet on this. I bet that he would actually stay in office. He did, and Kim Jong-un-

Robin: Well, we have a more dramatic example of that in the US presidential betting markets. You might know the chance of Biden at the moment is like 20% being the next president-

Richard: Yeah.

Robin: ... which the chance of Trump is 30% right? But Biden is the president right now and Trump lost the last election, so why would the Biden odds be so low? Well, the story is he might die, or become obviously-

Richard: Yeah, I think people also think-

Robin: ... incompetent and then not a candidate.

Richard: Yeah. I think it’s some combination of... You know it’s funny because the market has been underestimating Biden for a really long time, or at least in my opinion underestimating him, or betting against the market. I’ve been winning, but yeah even when he basically wrapped up the nomination it gave him a 70% chance of being the nominee which I thought was ridiculous.

It also always overestimated the chances I thought of Trump dropping dead, not just when he had COVID because there was that brief period where it looked like he could actually die. He was in the hospital…

Robin: Let’s just pause and notice. It’s quite possible to look at these prices and say, “Well, that doesn’t look right,” just like you can read a newspaper article and say, “That doesn’t sound right,” or any other analysis anywhere else right? Why am I recommending these market prices compared to anything else? Well, first of all there is this track record they do better, but there’s this other argument which says, “Okay. If you read the newspaper article and you think it’s wrong what can you do about that?” You can just complain. If you look at the betting market price and you think it’s wrong-

Richard: Yeah, exactly.

Robin: ... you can make money going, betting against it and fixing those prices. That’s the engine that makes them more accurate is all these people that can be enticed and invited to come fix the problems.

Richard: Yeah. Exactly. Yeah. I bet on Biden not dying, and Trump not dying, and both of them making it to election day. Yeah. I made money off of that. [Laughs]

Robin: There you go. I’m not going to certainly argue about that no one could ever find a mistake in these things. The question is when you can find a mistake in things which institution gives you the best opportunities to fix it?

Richard: Yeah. And you can compare the betting markets to, just like punditry, because when I listened to pundits they never gave Biden a chance either so it’s not like the pundits were all saying it’s going to be Biden. I remember most people were talking…

Robin: Let me at this point admit what I would say is the biggest problem with futarchy and with some of these other decision markets, which is that they make hypocrisy harder, which is actually a problem. You might think, “Well, hypocrisy is a bad thing. Making it harder is good right?” Well, let’s walk through that.

At the moment, say ordinary people can claim to love trees and they just care a lot about trees. Trees real estate wonderful and they certainly wouldn’t want to have fewer trees. But then they elect politicians who have to make choices about trees versus other things. Those politicians can probably read the public and say, “Well, they say they like trees but they don’t really like trees that much, so I’m not actually going to go save some trees by interfering with something else.”

Then if the public ever finds out that somehow not everything was being done to save trees, the public can complain and say, “That damn politician! They’re corrupt! They were bought out and I sure hate them. Let’s throw them out of office,”right? Because the politician is allowing the public to be hypocritical, to pretend they care more about trees than they do.

This happens all through the political system. For example we have laws against prostitution that we don’t enforce very well, which allows a lot of prostitution so people can have prostitution and then pretend they’re against it. Same thing with drug laws. A lot of our laws are in some sense to allow the public to pretend to have certain positions that they don’t really have.

The prediction markets, the futarchy decision markets don’t make that so easy. That is if in the national welfare definition you put a high weight on trees, then the speculators are actually going to approve the policies that do get you more trees. If that’s not what you wanted then you won’t be happy.

Richard: Yeah. But I mean there’s such a step removed when you’re talking about voters and what they want right? They want trees…

Robin: But I think it’s... Even when we talked about the example of hiring people. You have a couple of job candidates and you want to hire the best one for the company supposedly right? Well, I think actually when a person volunteers to be in charge of a hiring committee they don’t actually intend to pick the best person for the company. They intend to pick the best person for their coalition in the company.

Forcing these metrics of who is best for the company would interfere with their plan to pick someone who is decent for the company but even better for their coalition. That’s just the sort of thing that happens in many organizations. You would be uncomfortable setting up this process that didn’t give you the flexibility to pretend to do A while really doing B.

Richard: Yeah. Changing gears a little bit do you think that perhaps a foreign country, perhaps some kind of dictatorship might be more amenable to these kind of things? Because think of it this way. They’re often looking for a sense of legitimacy, a reason for status that is not based on the dominant culture which says you need elections, and you need democracy, and you need popular legitimacy.

Robin: I think to answer this we have to realize that there is a world elite culture. This was very striking to me at the beginning of the pandemic a year and a half ago. At the beginning of the pandemic the usual public health experts took their usual positions say against masks, and against travel restrictions, and things like that.

Then this looked like an important thing and all the sudden elites everywhere started talking a lot about the pandemic and discussing what they thought was the right thing to do, and they decided something else. They came up with a different plan with lock downs, and masks, and things like that. Once the elites had decided on that all the public health experts caved and said, “Oh, yeah. Yeah. That’s what we should do.”

Not just in the United States or Britain. All around the world. Remarkably the policies adopted around the world have not varied that much from what the elites together around the world recommended. If you looked in other areas of policy like nuclear energy, or electromagnetic spectrum, drug regulation, policies around the world don’t actually vary that much.

There is some sort of world culture that talks and decides what the right thing to do is. Then everybody does it. There really aren’t very many exceptions. A remarkable thing was that early in the pandemic many of us wanted there to be challenge trials where we would test vaccines quickly and effectively, or even test something like the regulation, and basically nowhere in the world did they allow challenge trials.

Only say recently in Britain have there been the first challenge trials, because just medical experts everywhere. You might think, “Why didn’t some dictator somewhere want to be a hero by defying the world medical ethics experts and doing it different?” None did, right? That really suggests that dictators around the world more crave the approval of the world elites in doing things the way the world elites want to, and their political power at home is more strengthened by appearing to follow along with what the world elites say.

Richard: Yeah. Political science, they call this a logic of appropriateness, and this is what guides government behavior. Although China sort of did that. I mean what China did was go much harder on lockdowns and much harder on mass testing than other people.

Robin: Right.

Richard: That was a limited extent but they didn’t do human challenge trials to my knowledge. But they did do things that were different…

Robin: It’s important to notice there is variation in regulation of the world, but it’s also important to notice how limited it is.

Richard: Yeah. It’s within a narrow range. That’s true, yeah. You see this on social issues. You see like Black Lives Matter protests in New Zealand, and you see LGBT flags. All the countries in the world decided that gay rights was important at pretty much the exact same time.

Robin: This was really a problem for large social innovation. I’ve really over my life thought about lots of big ways we can make big changes to a lot of social institutions, but in a world like this where everybody wants to do what everybody else is doing it’s really hard to get anybody to try any big changes.

Richard: Is an answer to this perhaps geopolitical tension? If the US and China become best friends, maybe they converge, if they hate each other maybe they do completely different things? Could this be a hope that you have international tensions and you have these blocks, and then at least people do different things?

Robin: I don’t know, but a lot of people have mentioned recently how badly say the US Military managed in Afghanistan for several decades. They compare that interestingly to how flexible the US Military was in World War II after a bunch of big losses early on. The remarkable thing, the US Military at the beginning of World War II was not very well run and not very well organized. They had lousy suppliers and things.

Then they made a bunch of big losses early on. Then they thought it was important enough not to keep doing that so that they fired people and fired suppliers. They now put performance as a priority because it was a big war. Apparently that’s the kind of thing it seems to require. But the pandemic apparently wasn’t such a thing right?

Richard: Yeah.

Robin: The pandemic was not a big enough crisis that we fired people who did badly on it. Neither was Afghanistan. We’re in a world where we have these big things we do wrong but they somehow just aren’t bad enough to really scare us into trying different things. The question is where will we ever see some nation or big organization that’s scared enough about losing to be willing to roll the dice and try some big changes?

Richard: When you look at the American Military established under World War II I mean the military establishment was a new thing. You were building basically something from scratch. Now you have all these vested interests. You know it’s funny. The places, the countries with the most US Military… the most military personnel in the world are actually Italy, Germany, Japan, and South Korea right?

Robin: Those are risky, dangerous spots. You’d want troops there wouldn’t you?

Richard: Yeah. Well, maybe but if you notice they have something in common. Those are the Axis powers and the Korean War right?

Robin: Right.

Richard: Basically they’re the exact same place they were in 1945 to 1950 and so-

Robin: Hysteresis right? Enormous path dependence?

Richard: Yeah, exactly. Enormous dependence. Yeah, Italy. Is that obvious? The most dangerous place in the world. Maybe, maybe not.

Robin: No, and it’s not remotely obviously the most dangerous place in the world.

Richard: Yeah. Do you look around the world, and right now do you see variation in the extent to which countries are willing to not only take risks but take risks specifically along the path that you suggest?

There was an article in The Economist earlier this year. I don’t know if you’ve seen it, but the UK, the intelligence agencies have a prediction market but it’s called Cosmic Bazaar. I actually googled it and I couldn’t find it. If you can’t find it on the first page of Google then that’s not a good sign.

Robin: Right. The US intelligence agency has also had an internal prediction market going for a while. They’ve had this interesting way they handle it politically. Inside the CIA the coin of the realm is reports, or analysis. Somebody writes a report that analyzes a particular place like Italy say, and summarizes the key strategic situation there, and the key intelligence situation.

There are these betting markets that exist where people can bet and forecast on these things. But the rule is they don’t cite the betting market in their reports. The market doesn’t get credit for influencing the reports, although it probably does influence the reports. That limits the degree to which it gets budget or attention because why bother to bet in the market if you’re not going to get credit there?

Richard: Yeah. Yeah. There is a paper coming from the intelligence agencies that compared super forecasters and people who had proven some track record versus people in the intelligence community with access to classified information. Phil Tetlock showed me this paper. Yeah. You could probably guess what happened.

The intelligence community lost to the people with the track record of forecasting. You could see why the intelligence community might not want to hype up this result. It seems like there is a lot of data out there-

Robin: Right. Clearly the intelligence community is basically saying, “Yes, we know we could get more accurate estimates from that but we don’t want them. We like our current system,” right? If they were scared that might turn out different right?

Richard: If they were scared of China, yeah, taking…

Robin: Right. Some external threat. The same thing was true about my betting market publicity fiasco in 2003. This was soon after 9/11 and just two years later. People looked at the betting markets and said, “Oh, you’re betting on death. That’s terrible. You have to shut them down.” If they were really scared of terror attacks, if they were actually feeling a large degree of threat they would have said, "To heck with this rule against betting on death. Let’s turn on these markets. Let’s find out where the attacks are going to be so we can stop them."

Richard: They say Bin Laden is just going to put all his money in the market and then attack?

Robin: Well, that was crazy because these were relativity thin markets, and they have a lot of money at stake. Basically a fact that people don’t know about the markets is that many people criticize by saying, “Well, somebody will try to manipulate the markets by betting on one side not because they know better, but because they’re willing to lose money in order to distort the market price.”

That is true. There are people willing to manipulate markets, but that actually makes the prices more accurate. For example in the fire the CEO market you say, “Well, the CEO wants to keep his job, so he will bet in these markets in order to make himself look like the price will be higher if he stays, and lower if he leaves.”

Yes he would have an incentive to do that, but when other traders know that somebody will be trying to manipulate in the market they know to increase their trading and their efforts and that compensates, and actually on net makes the prices more accurate. That’s something we see in theory and we’ve seen in the lab, and we’ve seen in the field. These markets are robust to attempts to manipulate. In fact people who want to manipulate them make the prices more accurate.

Richard: Yeah. Do you think that one way to think we should do is raise the status of thinking about these things, and thinking about betting markets? Because it seems like there is data out there. I mean you could go onto the stock market. We’ve talked about predicted. You can go back to elections.

You can calculate some kind of conditional probabilities. Do you think a good thing could be just have more economists just interested in these questions, and looking at data, and comparing studies?

Robin: It couldn’t be bad, but the question is just how much hope should you have? That’s a key question about a lot of institutional choices. Honestly if you just look at institutional issues in the United States or other countries and you ask which kinds of choices do people get really excited about, and emotional, and interested in, if you tell them about a policy change that would just benefit most everybody they yawn and can’t be bothered to pay attention.

They would just lose interest right? If you tell them about a policy change that will help their side and hurt the other side ooh, they just love that. People are really eager to fight in a battle. A lot of the topics that energize them are the topics that represent a conflict between one group and another group. That means institutional changes are just boring because even if you can find out a better institution it just doesn’t map onto their side versus the other side.

Richard: Yeah. Maybe that gives me an idea for an investment idea. You see these things in the conservative press. They’re talking about some corporation has gone woke right? They have a Critical Race Theory or trading in Coca-Cola or whatever. Basically you could have some kind of mutual fund that just shorts the wokest companies, whoever could short whoever Fox News happens to be complaining about at the time-

Robin: Right. And that would be a way in which you are taking a side. Then that would be more energizing to people. People would just like to-

Richard: Right. Or you could invest-

Robin: ... take a side.

Richard: You could invest in those corporations. Right.

Robin: Right.

Richard: Exactly. Then eventually you would learn if this thing lost money year after year you’d learn something…

Robin: Sure. And in fact ordinary people would be more interested in betting on the stock market if they could simultaneously be taking a political side with their stock market bets, which is…

Richard: But they can. Yeah. Right now we have all these outrages over some corporation is doing this or that, so you’d figure... I wonder if that’s actually inspiring more people to get into the stock market? It’s hard to tell with Robinhood expanding, making it easier. But you could imagine some entrepreneurs doing that right?

You could imagine somebody setting something up and advertising to people, “ We’re going to short all the woke corporations.” You could imagine them doing well.

Robin: Right. The fundamental problem is how do you create, or find a created community that just cares about overall benefit of a nation, or a company, or things like that? Unfortunately one of the main ways that’s ever happened is war. We talked about World War II a bit before.

There’s a literature that suggests that war has been one of the main engineers of innovation for the last 10,000 years which is a terrible fact because it means if you want more innovation you’ll have to have more war. War is just terrible thing.

Richard: Yeah.

Robin: But all this time of peace and prosperity we’ve had for a while here, we also do seem to see a degradation in our interest in coming together for overall collective benefit, and more focus on internal divisions, and more focus on just doing whatever helps us in these little local battles and not caring very much about the overall nation because we’re assuming that’s okay.

Richard: Yeah. Well, you see nationalism manifest itself at say soccer games, like Germany and France are not fighting wars but they’ll go to soccer games. There’s this hooligan culture in Europe where people really, really get into it.

Robin: Right. But would they be willing to change some key national policy in order to make sure they could win more soccer games?

Richard: I think it would have to be... I think the class of the people who makes the policy is different from the soccer hooligans right? It would just be a matter of the elites having some kind of national pride. It doesn’t even have to be national. Could it be just a class pride, or a pride in background, you know these aristocrats?

Before there was mass nationalism there was war right? There was these aristocrats and they had their own value system. They had their codes of conduct.

Robin: Well, I mean the key thing would be say if the elites of Romania for something want Romania to look better in the world’s eye and try to make Romania be run better overall, that could be an energy that would focus on overall quality of Romania as opposed to the left elites in Romania fighting the right elites in Romania right, and being in a battle of taking down the other side.

Richard: Yeah. It sounds like what’s really dangerous is there’s this global elite culture where it’s not just public health. It’s like on social issues, on just...

Robin: Right. They have strong consensus in you just have to follow the global elites to be part of them. There’s not so much competition within those global elites in that sense for doing things effectively.

Richard: Yeah. The competition is just the less well off people in their own countries-

Robin: If you think of say, Elon Musk say, right, if the global elites go, “Tsk, tsk Elon Musk,”and say, “Well, he’s not doing it right. He needs to follow these regulations right,” and then Elon Musk is actually making things better, and making a better internet and a better space industry or whatever, well does Elon Musk... If he wins does that change the elites to be more supporting him, or do they just get more mad that he defied them and he seems to be winning?

Richard: Yeah. What do you think about the potential? There’s a lot of people in Silicon Valley people and the crypto world, people like my friend Balaji Srinivasan and Mark Andreessen, and people like this who really take a dim view of the Davos set, the New York Times read in public. I don’t know if they see themselves this way. I’m not speaking for anybody, but that could potentially be a kind of counter elite right?

Robin: And the danger is that if the regular elites see this defiant group of tech elites winning against them that makes them really mad and wanting to take them down.

Richard: Well, that’s the risk of competition right? The good side, or the more productive side could lose, right? But if we’re thinking about how to have competition and how to... If we’re not going to have wars, if we’re not going start wars then…